Clear Lake homeowner Bob Dempsey learned in 2023 that his home insurer Kemper was leaving his area. Dempsey signed up for a new policy with SageSure-at more than double the cost of his previous policy.

"The rising home insurance premiums are a big problem, and there's no explanation from companies about why they aren't covering my area," Dempsey said.

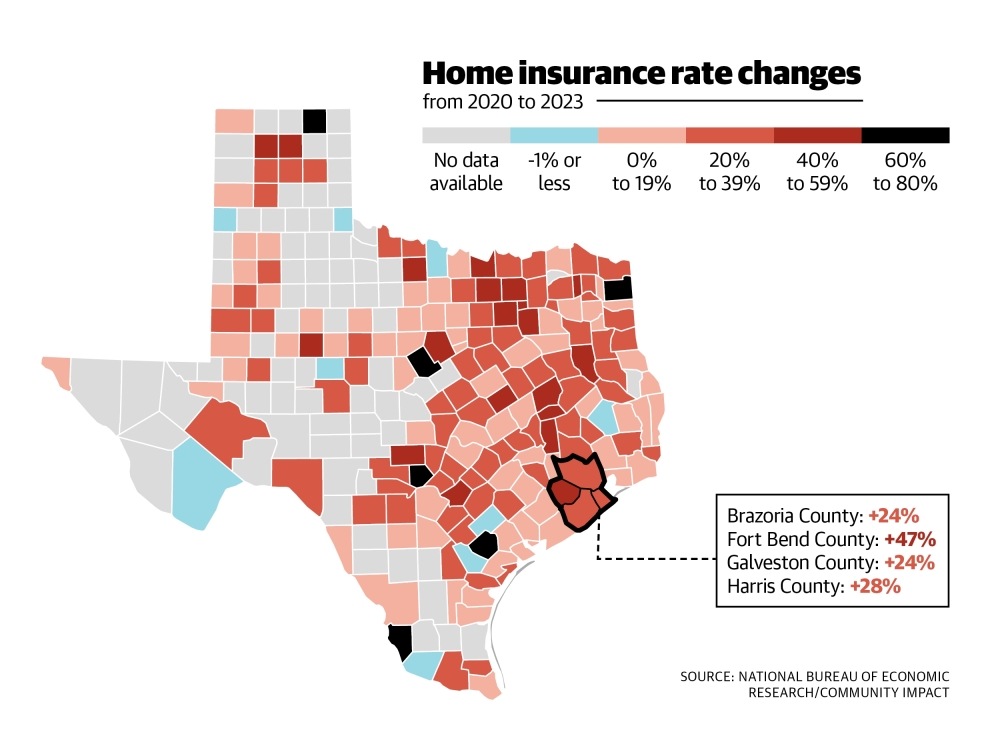

The Greater Houston area ranks near the top of the list for the state, causing some in the Pearland-Friendswood area to forgo insurance altogether. Meanwhile, some insurance companies are leaving the market due to risk.

The background

Since 2003, Texas has used a file-and-use system for home insurance, which allows insurance companies to issue higher rates without state approval so long as they notify the state, according to the Texas Department of Insurance, or TDI.

These are referred to as “drive-by-filings,” said Ware Wendell, executive director of Texas Watch, which is an organization that monitors insurance practices in the state.

“They could just slide an envelope across the desk at [Texas Department of Insurance] and tell them, ‘This is what we’re charging,’ and then put that into practice immediately,” he said.

It’s incumbent upon the TDI to challenge hikes that don’t comply with state law, Wendell said. Of the more than 2,300 rate filings the TDI reviewed in 2024, none were disapproved, according to the TDI.

From 2022 to 2023, insurance premiums in Texas increased by 23%, marking the highest rise in the nation in that timespan. This compared to the national average increase of 11%, according to a report from S&P Global, a company that specializes in information and analytics around finance and business.

John Cobarruvias, a consumer advocate and Clear Lake homeowner, said he feels price increases from contractors are a cause for rising insurance costs for policyholders. Costs of repairing items such as roofs or other structural aspects of a home have risen over the past decade, he said, which in turn drives up the costs of insurance.

“The roofing company charges that large amount, the insurance company pays that large amount and then we get charged for it in their premiums,” he said.

To help solve the issue, the state is looking at some bills in the ongoing legislative session, such as House Bill 2067 from Rep. Dennis Paul, R-Clear Lake, which would require insurers to provide a reason for when they decline, cancel or don’t renew a policy.

Other help comes through the Texas Windstorm Insurance Association, or TWIA, which is a state-sponsored insurance provider for homeowners who can’t obtain a policy from private insurers.

The number of polices written for homeowners in Brazoria and Galveston counties through TWIA has increased by at least 36% in each county dating back to 2019, according to TWIA data.

The conditions

In Texas, 160 companies offer homeowners insurance policies as of 2025, which has remained steady since 2022 and is a 20% increase compared to a decade ago, according to the TDI. In 2023, insurance companies sold more than 8.7 million policies in Texas—up 35% from 2013.

Still, insurance companies are struggling in Texas, according to filings from multiple insurance companies. In 2022, the San Antonio-based United States Army Automobile Association, or USAA, reported its first loss in its 102-year history, according to the insurer’s 2022 annual report.

Other insurance companies are limiting the policies they write in Texas, filings show.

“Our advice to consumers is to keep shopping,” TDI Communications Specialist Ben Gonzalez told Community Impact in an email.

How it works

Insurance companies have stated in recent news releases they’re facing many risks, such as natural disasters and the lingering impact of the COVID-19 pandemic on lumber and building costs.

Issues related to Hurricane Beryl, which caused billions of dollars in damage, as well as Winter Storm Uri in 2021, are creating upward pressure on premiums, said Stephanie Montiel, a Pearland resident and insurance broker at TWFG Insurance.

Higher premiums resulting from those issues are causing nonrenewal rates to climb in recent years, Montiel said. In December, the U.S. Senate Committee on the Budget published a report that compiled nonrenewal rates across counties in all 50 states.

The data confirms that the states and counties most vulnerable to climate-related risks, such as wildfires or hurricanes, have the highest nonrenewal rates and the most significant increases in these rates. Coastal counties such as Brazoria and Galveston counties fall into this camp, according to the report.

Bills to watch

Paul said he hopes HB 2067 will help hold insurance companies to account while also helping the state gather information as to why companies are dropping customers.

Some, such as Cobarruvias, said they don’t feel this approach will help because it doesn’t directly deal with rate increases. However, Paul said the state is limited in how it can address the issue.

Paul said he feels the state needs to incentivize competition to bring in more insurance companies, which he said would spread out the risk and therefore potentially lower rates. He said he believes the state setting direct rates or limiting increases could cause companies to leave.

“Having government interference come in and set a rate is a total disaster,” he said.

Separately, state Rep. Tom Oliverson, R-Cypress filed HB 1576 which would create a grant program for hurricane and windstorm loss mitigation for single-family residential property owners.

Final takeaways

Following Hurricane Beryl, TWIA officials asked to increase their rates by 10%, but the TDI blocked it, according to TWIA’s website.

In a December report, TWIA officials stated they expect Beryl’s claims could fully deplete the organization’s $450 million catastrophic reserve trust fund. TWIA’s website states the organization hopes to discuss in the 89th legislative session some potential changes in how it pays for storm losses.

Still, Cobarruvias said he is worried the TWIA is becoming the only insurance option for some homeowners.

“That was supposed to be the insurance of last resort,” Cobarruvias said.

In addition to his bill and others proposed, Paul gave some ideas for lowering rates. Those include fortified home perks, which would offer discounts for people who upgrade their homes to protect against disasters. The state could consider group insurance options to lower rates as well, he said.

From 2019 to 2023, see how TWIA policies increased:

In Texas, 160 companies offer homeowners insurance policies as of 2025, which has remained steady since 2022 and is a 20% increase compared to a decade ago, according to the TDI. In 2023, insurance companies sold more than 8.7 million policies in Texas—up 35% from 2013.

Still, insurance companies are struggling in Texas, according to filings from multiple insurance companies. In 2022, the San Antonio-based United States Army Automobile Association, or USAA, reported its first loss in its 102-year history, according to the insurer’s 2022 annual report.

Other insurance companies are limiting the policies they write in Texas, filings show.

“Our advice to consumers is to keep shopping,” TDI Communications Specialist Ben Gonzalez told Community Impact in an email.

How it works

Insurance companies have stated in recent news releases they’re facing many risks, such as natural disasters and the lingering impact of the COVID-19 pandemic on lumber and building costs.

Issues related to Hurricane Beryl, which caused billions of dollars in damage, as well as Winter Storm Uri in 2021, are creating upward pressure on premiums, said Stephanie Montiel, a Pearland resident and insurance broker at TWFG Insurance.

Higher premiums resulting from those issues are causing nonrenewal rates to climb in recent years, Montiel said. In December, the U.S. Senate Committee on the Budget published a report that compiled nonrenewal rates across counties in all 50 states.

The data confirms that the states and counties most vulnerable to climate-related risks, such as wildfires or hurricanes, have the highest nonrenewal rates and the most significant increases in these rates. Coastal counties such as Brazoria and Galveston counties fall into this camp, according to the report.

Bills to watch

Paul said he hopes HB 2067 will help hold insurance companies to account while also helping the state gather information as to why companies are dropping customers.

Some, such as Cobarruvias, said they don’t feel this approach will help because it doesn’t directly deal with rate increases. However, Paul said the state is limited in how it can address the issue.

Paul said he feels the state needs to incentivize competition to bring in more insurance companies, which he said would spread out the risk and therefore potentially lower rates. He said he believes the state setting direct rates or limiting increases could cause companies to leave.

“Having government interference come in and set a rate is a total disaster,” he said.

Separately, state Rep. Tom Oliverson, R-Cypress filed HB 1576 which would create a grant program for hurricane and windstorm loss mitigation for single-family residential property owners.

Final takeaways

Following Hurricane Beryl, TWIA officials asked to increase their rates by 10%, but the TDI blocked it, according to TWIA’s website.

In a December report, TWIA officials stated they expect Beryl’s claims could fully deplete the organization’s $450 million catastrophic reserve trust fund. TWIA’s website states the organization hopes to discuss in the 89th legislative session some potential changes in how it pays for storm losses.

Still, Cobarruvias said he is worried the TWIA is becoming the only insurance option for some homeowners.

“That was supposed to be the insurance of last resort,” Cobarruvias said.

In addition to his bill and others proposed, Paul gave some ideas for lowering rates. Those include fortified home perks, which would offer discounts for people who upgrade their homes to protect against disasters. The state could consider group insurance options to lower rates as well, he said.

From 2019 to 2023, see how TWIA policies increased:

- Up to 78,237 policies in Galveston County, which is a 36% increase since 2019

- Up to 45,478 polices in Brazoria County, which is a 45.8% increase since 2019