For each market, data from the Texas A&M University Real Estate Research Center shows an increase in the number of homes listed to sell and the average amount of time it takes for a home to sell.

Large spikes in demand that took off at the beginning of the pandemic—which helped contribute to the rapid rise in prices—have begun to wane, according to the data. Buda, for example, had a reported zero months of inventory available in May 2021, but by May of this year, that local market had nearly three months’ worth of homes.

Months of inventory are how long real estate agents estimate the number of homes available at any given time will take to sell.

“Historically, if it takes three months to sell your house, that’s not bad, but compared to a year ago when there were no homes on the market—even with a little demand—they were snapping up those houses really quick,” said Bill Chittenden, an associate professor of finance at Texas State University. “More folks are wanting to sell their homes. But they’re on the market longer because it’s not as affordable as it was just a couple years ago, so it’s going to be harder for them to sell their homes.”

Affordability wanes

The rise in home prices, combined with recent hikes in interest rates, created an environment in which a large segment of the population is being priced out of the real estate market, said Stephanie Ryan, the president of the Four Rivers Association of Realtors, which focuses on the real estate market in Caldwell, Comal, Guadalupe and Hays counties.

From May 2020-May 2022, the median home price across Hays County rose from $265,900 to $470,000, or nearly 77%. The most recent data from the Realtors association shows it fell in May 2023 to $400,000.

“It’s pricing people out of the market,” Ryan said. “[If someone] could afford a more expensive home because your interest rate was so low, now it’s very difficult for people to do that.”

Even with Federal Housing Authority loans as an option for first-time homebuyers, covering the lower down payment and closing costs on a home can be a steep price tag, Ryan said.

The increase in interest rates by the Federal Reserve compounds the price of the monthly total payment on a home, meaning someone who could budget for a mortgage payment on a $369,000 home two years ago—the most current median home price in San Marcos—might not be able to afford it now as the monthly cost is significantly higher, Chittenden said. The most recent mortgage rates from Freddie Mac show 6.71% on a 30-year fixed-rate mortgage. In May 2020, interest rates hovered at or below 3%.

“Say the mortgage is $350,000. ... That difference between the [principal and interest] payment today and the [principle and interest] payment two years ago is a $750 difference,” he said.

Chris Kerr, a loan officer with Legacy Mutual Mortgage, said he is seeing fewer first-time homebuyers.

“Most of my buyers are move-up and move-in, so there are people moving up at home, or they’re moving in from out of the area, so they’re coming from higher-priced areas buying homes here,” Kerr said. “I got a guy in California right now; I got a guy from Montana, a guy from Corpus [Christi]. ... It’s not the first-time buyer or the lower-income, lower price point.”

Market beginning to balance

While the months of inventory figure is extending in local markets, real estate experts cautioned the market is not yet balanced. Listings on the market and the average number of days to close keep growing, but local markets are still favoring sellers, keeping prices up, they said.

According to the Texas A&M Real Estate Research Center, six to 6 1/2 months of inventory in a market is considered a balanced market. San Marcos, Buda, Kyle and Hays County are hovering around three to four months of inventory as of May.

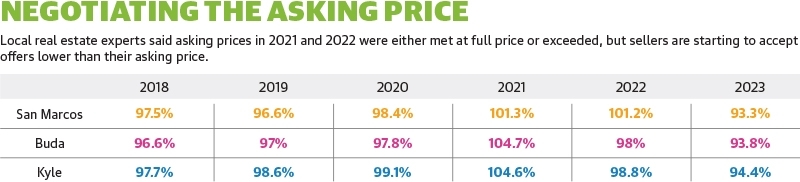

Ryan said she believes the median price is still up because there is enough pent-up demand in the area, and sellers are trying different methods of negotiating prices rather than starting at a lower asking price.

One trend that might illustrate this best is the ratio of the closing price to the original price, Ryan said. Two years ago, data from the Realty association showed sellers in each market receiving more than the original asking price. Now that ratio is down to 93%-94% in each market, indicating concessions are being made.

“You’ll see people talking a little bit with us in terms of paying for some of the buyers’ closing costs or buying down their interest rate, maybe even for just a couple of years because they think [interest rates] are going to go back down again, or they do a permanent buy-down so the sellers [are in a] more competitive price range,” Ryan said.

Creating alternatives

Sellers and homebuilders are trying various methods of getting people in homes, including concessions, Kerr said. Seller concessions involve the seller giving the buyer money to use toward fees—or closing costs on a real estate transaction—and that can be part of the negotiation upfront on the contract and used in different ways to bring down monthly payments, he said.

One way to do this is through the seller buying down closing costs if the buyer needs to hang onto some cash because there is agreed-upon remodeling work needed on the property, he said. Another is through permanent or temporary buy-down of the interest rate by the seller.

“Utilizing that money to buy down the rate saves you long term because your payments lower, obviously. And that’s the pinch point for people is the higher monthly payment,” Kerr said.

But even with wiggle room on that front, many potential buyers are still priced out of the market, said Linda Jalufka, a Realtor with the Damron Group in San Marcos.

“Even though there’s people moving in in droves, a whole lot of them cannot afford a mortgage,” Jalufka said.

Homebuilders have the ability to work with their lenders, a title company, and insurance and construction companies to subsidize prices.

“And the resales cannot compete and have difficulties competing with that,” Jalufka said. “We’re seeing builders offering 4.9%-4.5% in the market, which is a good 2% to 3% lower than what they would qualify for without those subsidies. That changes your pricing in that section of the market.”

Another area is an increase in single-family homes that are either converted to rental properties or built out to be entire rental subdivisions, real estate experts said. Chittenden said there is a trend of large private equity companies buying single-family homes to turn around and rent them.

In 2022, a report from the National Association of Realtors revealed 28% of homes purchased in Texas the previous year were from institutional investors, the highest in the nation.

“The percentage of homes that were sold that were bought by these private equity firms over the last couple of years was surprisingly high,” Chittenden said. “I think for some folks, particularly over the last couple of years, that’s added to the pressure of them being kind of pushed out of the market. That [pressure has] combined with higher interest rates and these private equity firms buying up those properties.”