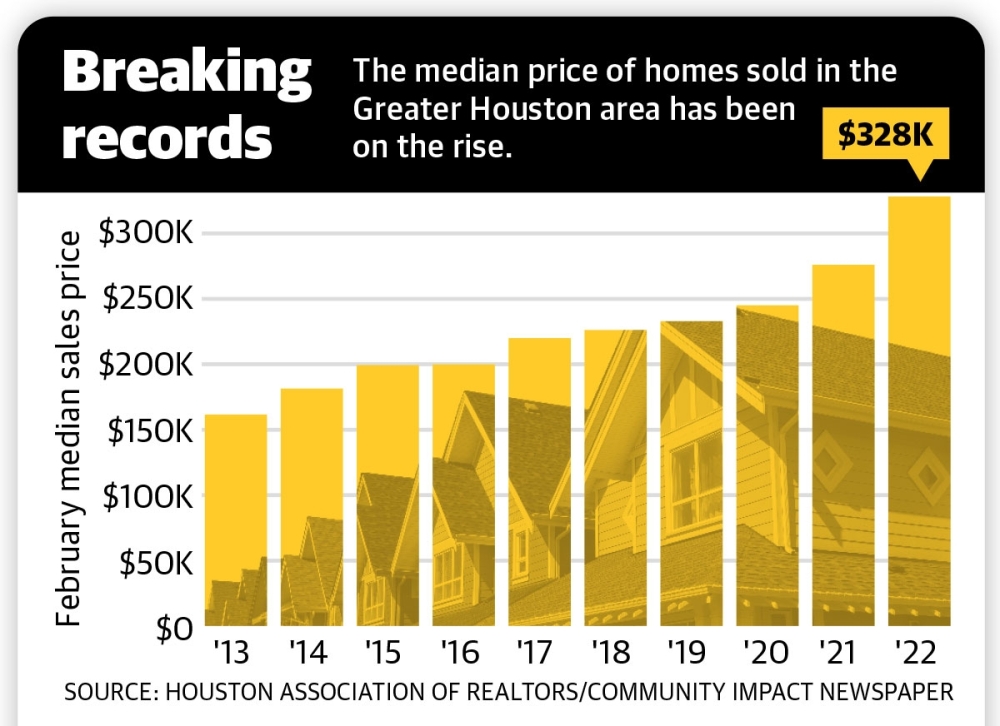

That trend can also be seen in the Greater Houston area, where the median price of single-family homes sold has risen by more than 30% since the start of the pandemic in March 2020, according to the Houston Association of Realtors. The median price hit $328,000 in February of this year, up from $245,000 two years ago.

Market experts said the rise in home prices can be partially tied to economic inflation, which has impacted nearly every market in the U.S. However, inflation alone does not answer why prices have hit all-time highs, said Patrick Jankowski, senior vice president at the Greater Houston Partnership, an economic development organization in the Greater Houston area.

“The demand has gotten so strong, it’s driven up prices,” Jankowski said.

In 2021, 106,229 single-family homes were sold in the Houston area, according to the HAR, up from 96,271 in 2020. The costs of land, materials and construction labor have also increased, making it difficult to build a home for under $250,000, Jankowski said.

“The prices and the inflation, the disruption in the supply chain and the lack of materials, the lack of the labor, ... that is the most troublesome thing,” said David Jarvis, senior vice president at John Burns Real Estate Consulting, which has an office in Bellaire.

About 31% of Houston-area homes sold in 2021 were at or below the $250,000 price range, Jankowski said.

Widespread demand

A new generation of homebuyers has been entering the market as many second-time homebuyers have begun looking for new homes, Jarvis said.

“We’re seeing a lot of young professionals stick around because of the [Texas Medical] Center,” said Timothy Shanahan, a Realtor in the Meyerland area.

This rise in home sales is not exclusive to any single part of Houston, data shows. The city’s suburbs and urban areas are both highly active.

In the Brays Oaks area, the median home sale price rose from the $150,000-$200,000 range in 2018 to the $200,000-$250,000 range in 2021, according to data from the Texas Real Estate Center at Texas A&M, peaking at $280,000 in December.

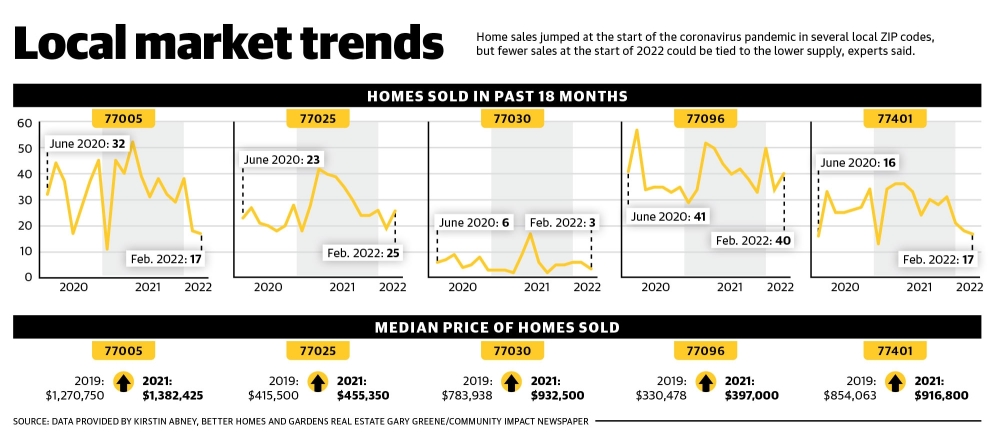

In smaller, more affluent cities, such as Bellaire and West University Place, the month-to-month trend is more volatile. However, the median price of homes sold in five ZIP codes in the Bellaire-Meyerland-West University area rose between 2019 and 2021, according to neighborhood data provided by Kirsten Abney with Better Homes and Gardens Real Estate Gary Greene. Homes in the 77096 ZIP code saw a 20.1% increase, from $330,478 in 2019 to $397,000 in 2021.

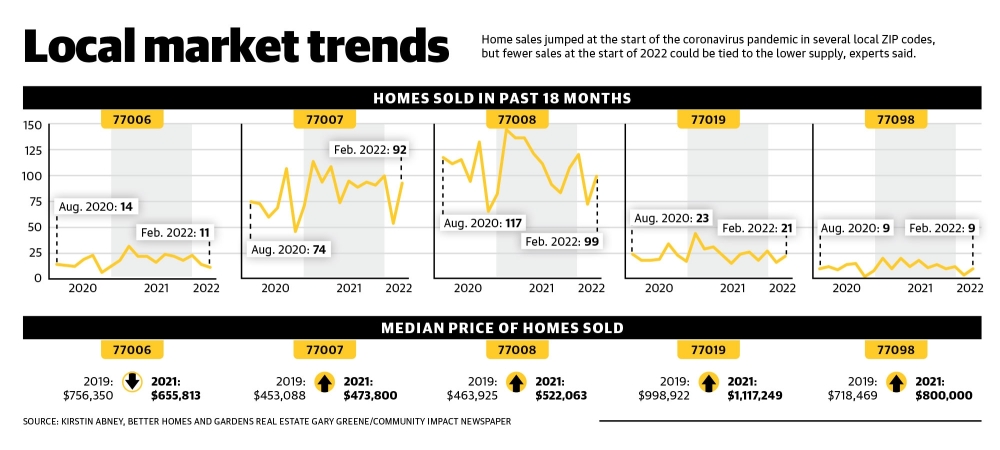

The median price of homes sold in four of five ZIP codes in the Heights, River Oaks and Montrose area rose between 2019 and 2021. The median price rose by more than 10% in the 77008, 77019 and 77098 ZIP codes over that time. The 77006 ZIP code, which covers parts of Midtown, saw a drop in median price over that time of roughly 13%.

Meanwhile, monthly data from the Texas Real Estate Center at Texas A&M University shows the median price of homes sold in the Greater Heights in 2019 rarely topped $500,000. Throughout 2021, the median price was over $500,000 in every month except February.

Cameron Ansari—a Realtor with Greenwood Properties who tracks trends in River Oaks, Montrose and West University Place—said the lack of housing inventory is the primary driver of market trends right now, forcing people to fight over the few houses available.

“There are all these buyers at every new listing’s open house,” he said. “You can see them standing in the front yards with their Realtors. It’s like a spectator sport.”

The low supply cannot be tied to low construction, Jarvis said. In 2019, 34,000 new homes were built in the Houston area, a figure that rose to 39,000 in 2020 and 43,000 in 2021. However, the demand still outpaced the supply, Jarvis said.

“The story is the same all over Texas and all over the country,” he said. “We built all we could.”

Over the course of the pandemic, the Federal Reserve began buying up mortgages to drive down rates and facilitate rapid growth in the market.

“We are going to go into a period where, kind of by design, demand [for] both new and resale will begin to decline as interest rates increase,” said Lawrence Dean, a Meyerland resident and senior vice president of advisory at Zonda, a company that specializes in housing market research and analytics.

“But because we’ve not been able to satisfy demand for so long, we got this sort of built-in wiggle room before demand could potentially decrease to when it’s below supply.”

Rise in interest

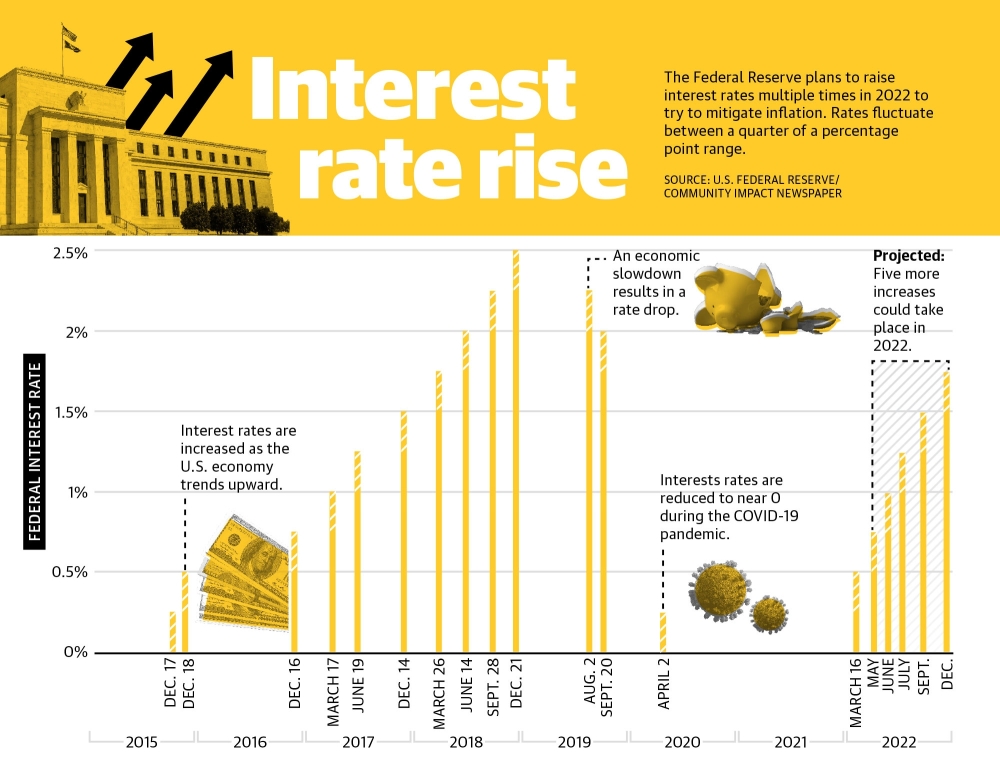

In April 2020, the Federal Reserve lowered interest rates to nearly zero to stimulate the economy as the coronavirus pandemic forced the closure of thousands of businesses nationwide, Jarvis said.

The Houston-area real estate market stayed strong throughout the pandemic despite supply chain issues, which allowed companies to raise prices on consumers, Jankowski said. The move to raise interest rates this year, potentially to 1.5% by December, is intended to reduce demand, he said.

“You raise interest rates to make things more expensive to purchase,” Jankowski said.

On March 16, the Federal Reserve raised interest rates for the first time since December 2018.

The change was a quarter of a percentage point higher from nearly 0% to 0.25% with up to six more similar increases planned throughout 2022.

An increase in the federal interest rate trickles down to a number of areas, including higher mortgage payments, credit card payments and interest rates on savings accounts. The effect on mortgage payments, in particular, comes with other concerns, Dean said.

“We are in an environment where moving up to a 4%-4.5% typical mortgage interest rate can actually begin to pose some problems and slow down demand for both new and resale homes,” Dean said.

In Harris County, the median monthly mortgage payment is more than $1,100, according to the Federal Reserve Bank of Atlanta. Because mortgages are taken out when homeowners cannot afford to buy a home outright, an increase in the mortgage rate would hit lower-income homeowners the hardest, said Clare Losey, assistant research economist with the Texas Real Estate Research Center at Texas A&M University.

“For a conventional loan on a $200,000 home with a 2.5% interest rate, a household needs to earn $51,954 annually,” Losey said in a March 16 news release.

With a 4% interest rate, the annual income needs to be near $57,954 for that same home, Losey said.

First-time homebuyers will also feel the brunt of the rise in interest rates, Dean said. However, homebuyers in the Bellaire, Meyerland and West University area are relatively less likely to fall into that category, he said.

Individuals who already own property are coming to the table with more equity, and monthly payments are not as significant a concern when purchasing a second home, Dean said.

Many home buyers in River Oaks are people looking to invest in an area where they see a lot of value, Ansari said. In Montrose, home buyers are often competing with speculative builders who are looking to make a profit, he said. A federal rate hike may slow down the home market in those areas, but the demand will always be there because of what they offer that few other locations in Houston can, Ansari said.

“Living in Montrose is close to all the cool things in town; that’s why people want to be there,” he said. “It’s all about lifestyle.”