According to a small business survey conducted by the Fort Worth Chamber of Commerce of more than 1,200 businesses in the area, the top concerns for business owners are revenue and cash flow; payroll and expenses; and rent or mortgage.

Nearly half, or 47%, of businesses in the area indicated a decrease in revenue by at least 60% since March 1, and 57% of businesses said they do not have company leave or remote working policies in place, which leaves owners and employees vulnerable to prolonged closures.

“We have been communicating with our members about different options,” said Barbara Walker, director of social responsibility and community involvement for Educational Employees Credit Union in Fort Worth. “We have some loan products that people are taking advantage of because they need to watch their cash flow.”

One primary component of the CARES Act is the Small Business Paycheck Protection Program.

The program allows eligible small businesses to apply for a loan with enough funds to cover up to eight weeks of payroll costs, including benefits. Loans are eligible for forgiveness if employers meet requirements for keeping employees on payroll, or hiring quickly, while maintaining salary levels.

Loans through the Paycheck Protection Program are also eligible to be used for interest payments on rent, mortgage and utilities as long as a minimum of 75% of the loan amount is used for payroll expenses.

“There are programs that people are realizing they need to leverage to get their financial house in order,” Walker said. “We are moving pretty fast and offering additional ways for people to get cash quickly and stabilize their financial situation.”

All small businesses with 500 employees or fewer are eligible for the Paycheck Protection Program, including nonprofits, veterans’ organizations, self-employed individuals and independent contractors.

In addition, all loans through the program will have the same terms, regardless of the lender or borrower.

Unemployment benefits have also been extended for self-employed workers and independent contractors to include an additional $600 per week for up to four months.

“We have been doing what we can, from a community perspective,” Walker said.

Walker noted additional options for businesses and individual customers, such as debt consolidation, mortgage and auto refinancing, hardship loans and skip payments, an option for existing borrowers to pause credit and mortgage payments.

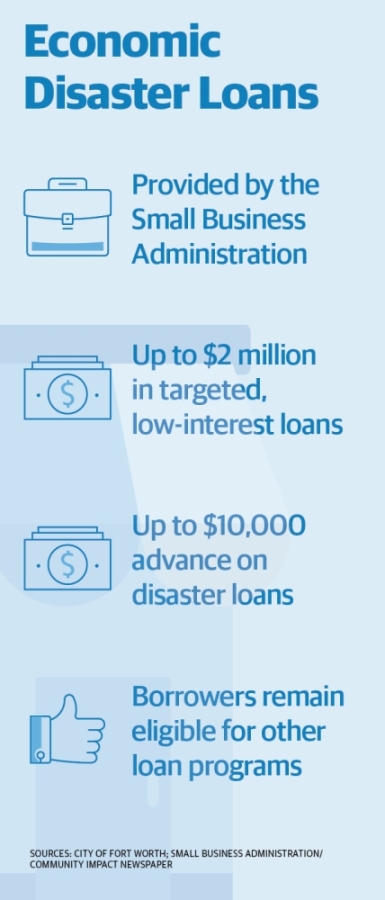

Another avenue of financial relief for small businesses is the U.S. Small Business Administration's disaster loans, which can provide up to $2 million in targeted, low-interest recovery loans.

Businesses across the state are eligible to apply for SBA disaster loans as of March 20, and with the passage of the CARES Act, businesses are eligible for an advance of up to $10,000 on SBA Economic Injury Disaster Loans.

The SBA provides alternative options for small businesses, such as the Express Loan Program, which provides up to $350,000 for no more than seven years, and the Community Advantage Loan Program, which allows mission-based lenders to assist small businesses with a maximum loan amount of $250,000.

More information on resources for small businesses is available here.