“It’s kind of outside of everybody’s control—you’ve got to have homeowners insurance, and you’ve got to pay property taxes—but these costs are, in Texas specifically ... getting extremely high,” he said.

Texas has some of the highest home insurance premiums in the nation, according to the National Bureau of Economic Research. These rates and the resulting cost are leading many to forgo home insurance altogether.

Laura Crain, president of Crain Insurance Group, which serves the Spring and Klein communities, said the problem is not only a Texas issue, but one that plagues homeowners nationwide.

Zooming out

Texas uses a file-and-use system for home insurance, which allows companies to issue higher rates without state approval as long as they notify the state, per the Texas Department of Insurance.

“They could just slide an envelope across the desk at [the TDI] and tell them, ‘This is what we’re charging,’ and then put that into practice immediately,” said Ware Wendell, executive director of Texas Watch, which monitors insurance practices in the state.

It’s incumbent upon the TDI to challenge hikes that don’t comply with state law, Wendell said. Of the more than 2,300 rate filings the TDI reviewed in 2024, none were disapproved, according to the TDI.

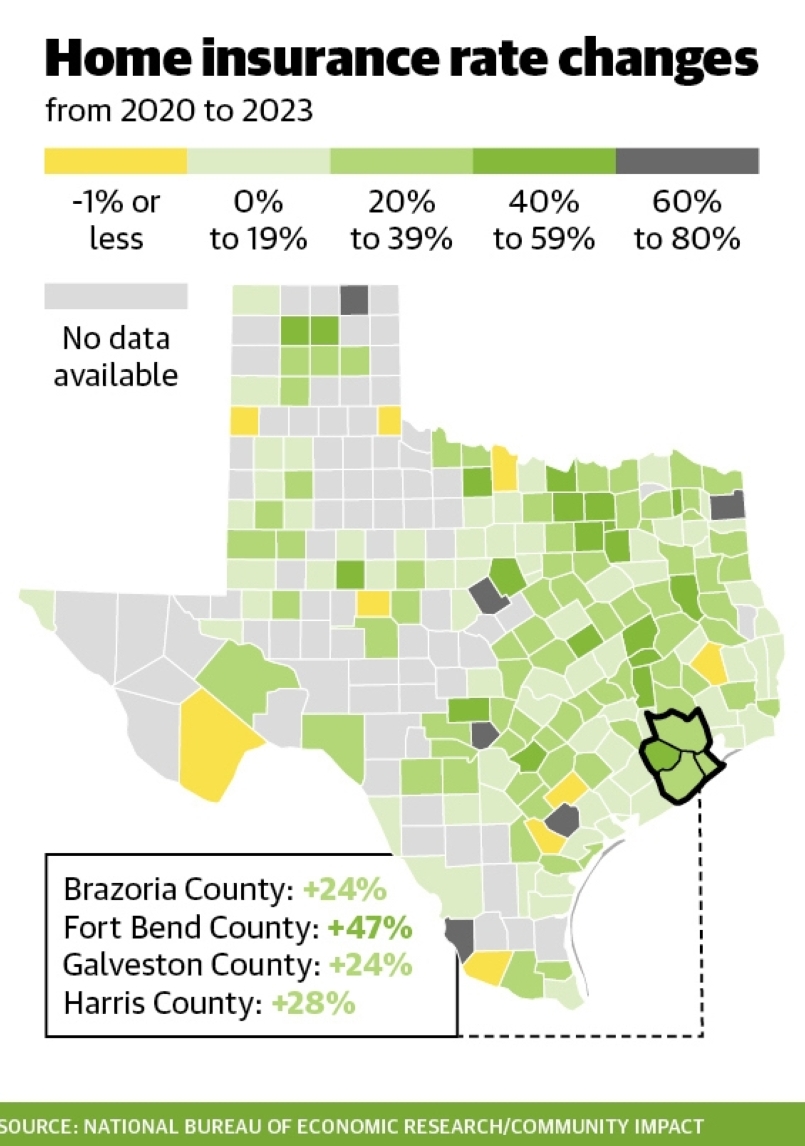

From 2022 to 2023, insurance premiums in Texas spiked 23%, compared to the U.S. average increase of 11%, according to S&P Global, which specializes in information and analytics around finance and business.

John Cobarruvias, a state consumer advocate, said he feels price increases from contractors are a cause for rising insurance costs for policyholders. Costs of repairing items such as roofs have risen over the past decade, he said, which in turn drives up the costs of insurance.

To help solve the issue, Gov. Greg Abbott signed House Bill 2067 into law on June 20, which will require insurers to provide a reason for when they decline, cancel or don’t renew a policy.

The conditions

In Texas, 160 companies offer homeowners insurance policies, which is a 20% increase compared to a decade ago, according to the TDI. In 2023, insurance companies sold more than 8.7 million policies in Texas, up 35% from 2013.

Still, insurers are struggling in Texas, according to filings from multiple companies. In 2022, the San Antonio-based United States Army Automobile Association, or USAA, reported the first loss in its 102-year history. Other companies are limiting the policies they write in Texas, filings show. How it works

How it works

Insurance companies have recently reported they’re facing risks, such as natural disasters and the lingering impact of the COVID-19 pandemic on lumber and building costs.

Carriers have increased the premiums of their policyholders nationwide; however, the Houston area has experienced dramatic increases as analysts deem the area “high risk,” Crain said.

“We are in what we would consider more of a high-risk [area], because we see a lot of natural disasters, you know, we have the wind and hail, we have the hurricane, we have the flooding, we have all of these different events that do impact our insurance,” Crain said. “So we are seeing rate increases.”

Like its predecessors, such as Winter Storm Uri in 2021 and Hurricane Harvey in 2017, Hurricane Beryl caused billions of dollars in damage last summer, according to property analytics firm CoreLogic.

In December, the U.S. Senate Committee on the Budget published nonrenewal rates, confirming areas most vulnerable to climate-related risks have the highest nonrenewal rates and the most significant rate increases. At the Capitol

At the Capitol

Gov. Greg Abbott signed HB 2067 into law on June 20, effective Jan. 1. Paul said he hopes the legislation will hold insurance companies accountable while also assisting the state in determining why companies are dropping customers.

Some, including Cobarruvias, said they don’t feel this approach will help because it doesn’t directly deal with rate increases. However, Paul said the state is limited in its ability to address the issue. Paul said he feels the state needs to incentivize competition to attract more insurance companies to spread out the risk and potentially lower rates. He said he believes the state setting direct rates or limiting increases could cause companies to leave.

“Having government interference come in and set a rate is a total disaster,” he said.

Looking ahead

According to a June 17 report from Rice University’s Kinder Institute of Urban Research, home insurance increases brought on by extreme weather events could add more than $15,000 to home costs.

Experts in the report recommend data-driven infrastructure planning and accurate flood risk mapping to address climate risks across Harris County, where more than 20% of all housing units are in major flood areas.

“The risk is going to continue to grow, and it’s really on us to figure out ... what we do with these spaces where we have so much infrastructure and economic investment and development in a place like Houston,” said Jeremy Porter, head of climate implications research at the nonprofit First Street.

Hurricane season tips from the TDI include:

In Texas, 160 companies offer homeowners insurance policies, which is a 20% increase compared to a decade ago, according to the TDI. In 2023, insurance companies sold more than 8.7 million policies in Texas, up 35% from 2013.

Still, insurers are struggling in Texas, according to filings from multiple companies. In 2022, the San Antonio-based United States Army Automobile Association, or USAA, reported the first loss in its 102-year history. Other companies are limiting the policies they write in Texas, filings show.

Insurance companies have recently reported they’re facing risks, such as natural disasters and the lingering impact of the COVID-19 pandemic on lumber and building costs.

Carriers have increased the premiums of their policyholders nationwide; however, the Houston area has experienced dramatic increases as analysts deem the area “high risk,” Crain said.

“We are in what we would consider more of a high-risk [area], because we see a lot of natural disasters, you know, we have the wind and hail, we have the hurricane, we have the flooding, we have all of these different events that do impact our insurance,” Crain said. “So we are seeing rate increases.”

Like its predecessors, such as Winter Storm Uri in 2021 and Hurricane Harvey in 2017, Hurricane Beryl caused billions of dollars in damage last summer, according to property analytics firm CoreLogic.

In December, the U.S. Senate Committee on the Budget published nonrenewal rates, confirming areas most vulnerable to climate-related risks have the highest nonrenewal rates and the most significant rate increases.

Gov. Greg Abbott signed HB 2067 into law on June 20, effective Jan. 1. Paul said he hopes the legislation will hold insurance companies accountable while also assisting the state in determining why companies are dropping customers.

Some, including Cobarruvias, said they don’t feel this approach will help because it doesn’t directly deal with rate increases. However, Paul said the state is limited in its ability to address the issue. Paul said he feels the state needs to incentivize competition to attract more insurance companies to spread out the risk and potentially lower rates. He said he believes the state setting direct rates or limiting increases could cause companies to leave.

“Having government interference come in and set a rate is a total disaster,” he said.

Looking ahead

According to a June 17 report from Rice University’s Kinder Institute of Urban Research, home insurance increases brought on by extreme weather events could add more than $15,000 to home costs.

Experts in the report recommend data-driven infrastructure planning and accurate flood risk mapping to address climate risks across Harris County, where more than 20% of all housing units are in major flood areas.

“The risk is going to continue to grow, and it’s really on us to figure out ... what we do with these spaces where we have so much infrastructure and economic investment and development in a place like Houston,” said Jeremy Porter, head of climate implications research at the nonprofit First Street.

Hurricane season tips from the TDI include:

- Shop for windstorm insurance if it’s not included in your home insurance policy.

- Consider comprehensive coverage car insurance, which covers vehicular damage from flood, hail, fire and wind.

- Have physical and digital copies of important documents, such as your policy’s declaration page and ID cards for auto and health insurance.

- Consider flood insurance sooner rather than later as flood policies usually take effect 30 days after purchase.

- Evaluate your home’s roof and windows; repairs and reinforcement ahead of a storm could save you money later.

- Take inventory of your home in case an insurance claim needs to be filed later.

- Build an emergency go kit stocked with water, food, medicine, clothes, pet food and other vital supplies.